Our financial life is not a mystery, it’s a puzzle we can solve. Credit scores, often seen as complex, are actually a key piece of this puzzle. Understanding them empowers us to take control of our financial future. In this piece, we’ll guide you through everything you need to know about credit scores, from what they are to how they’re determined and, most importantly, how to raise your own.

So, what exactly is a credit score? It’s not just a number; it’s a gateway to financial opportunities. Consider it a grade lenders use to evaluate your financial responsibility. The higher your score, the more doors open for you. It increases your chances of getting approved for loans and favorable interest rates, paving the way for a brighter financial future.

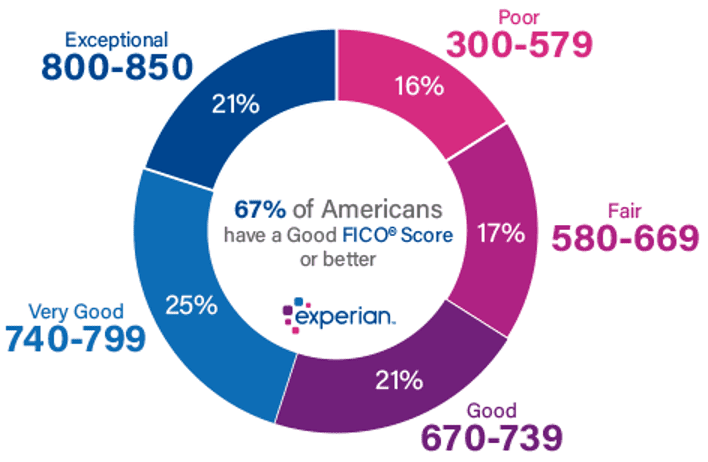

When it comes to credit scores, three companies are the big players in the US: Equifax, Experian, and TransUnion. They’re like the referees of your credit game. Each of them uses a slightly different scoring system, but they all play a crucial role in maintaining your credit history. They collect and maintain your credit information, which is then used to calculate your credit score. They look at the same things: your payment history, how much of your available credit you’re using, how long you’ve had credit, the types of credit you have, and if you’ve recently applied for new credit.

One of the most essential factors in determining your credit score is your payment history. It records your payment history, including any missed payments or accounts that went into collections. Paying your bills on time is critical because missed payments can significantly harm your credit score.

Another essential aspect of establishing your credit score is credit use. This refers to the amount of credit you are using compared to the total amount of available credit. For example, if you have a credit card with a $ 1,000 limit and you’ve used $ 500, your credit utilization is 50%. Using a significant percentage of your available credit may signal that you rely too heavily on credit, which lenders may regard as a red flag. The duration of your credit history is also crucial. In general, the more credit history you have, the better. It demonstrates that you have a track record of responsibly using credit over time.

Now that you know what factors influence your credit score, let’s discuss what you can do to enhance it. Paying your bills on time is one of the simplest methods to improve your credit score. You can set up automatic bill payments to ensure you never miss a due date. Another tip is to pay off high-interest debts first, as this can help lower your credit utilization and improve your score. Late payments can substantially negatively influence your credit score, so it’s critical to pay your obligations on time, every time.

In addition, it’s important to verify your credit reports frequently to guarantee accuracy. If you find any mistakes or inconsistencies, you can file a dispute with the credit reporting companies. This involves contacting the company in writing, providing evidence to support your claim, and requesting that the error be corrected. This process is crucial in maintaining the accuracy of your credit information.

Finally, understanding credit ratings and how to improve them is an essential component of financial management. You can take charge of your credit and increase your score by paying your payments on time, minimizing your credit card balances, and reviewing your credit reports regularly. Regular monitoring of your credit score is crucial as it allows you to track your progress and identify areas for improvement. It’s a proactive step towards maintaining a healthy credit score.